LIC Business - Vantage point from a Policyholder and an Investor

Hey! Hello Guys.

We have entered 2022 with a lot of headlines from the possibility of the third wave (Omicron) transmission to the Ukraine-Russia war but amidst this, our government has announced big welcoming news which is the entry of LIC (Life Insurance Corporation) into the equity market.

Well, it’s good news for LIC but what about the investors and policyholders who are considering participating or participating in it?

Let us analyze the business to find out whether it’s good news for investors and policyholders as well.

A study was conducted by the Boston Consulting Group and Morgan Stanley. The study of individual stock performance between 1990 – 2009 found that the primary drivers of stock performance are sales and (eventual) profit growth.

So now it’s very clear that we need to focus on the sales growth of any business.

What drives up the sales growth?

The underlying product or services which the business offers right?

Yes!

What type of Insurance products does LIC primarily offer1?

Endowment Plans:

Money-Back Plans:

Although LIC is offering Term Assurance, Rider, and Whole life plans they’re not highly incentivized for selling as compared to Endowment & Money back plans and it contributes a meager percentage of revenue2

Let’s focus on Endowment & Money back plans.

If you pay closer attention to most of these insurance products then you will start to sense there is something wrong with these products!

Yes, I am saying this for REAL.

Let us do the math and figure out whether my statement holds true or not.

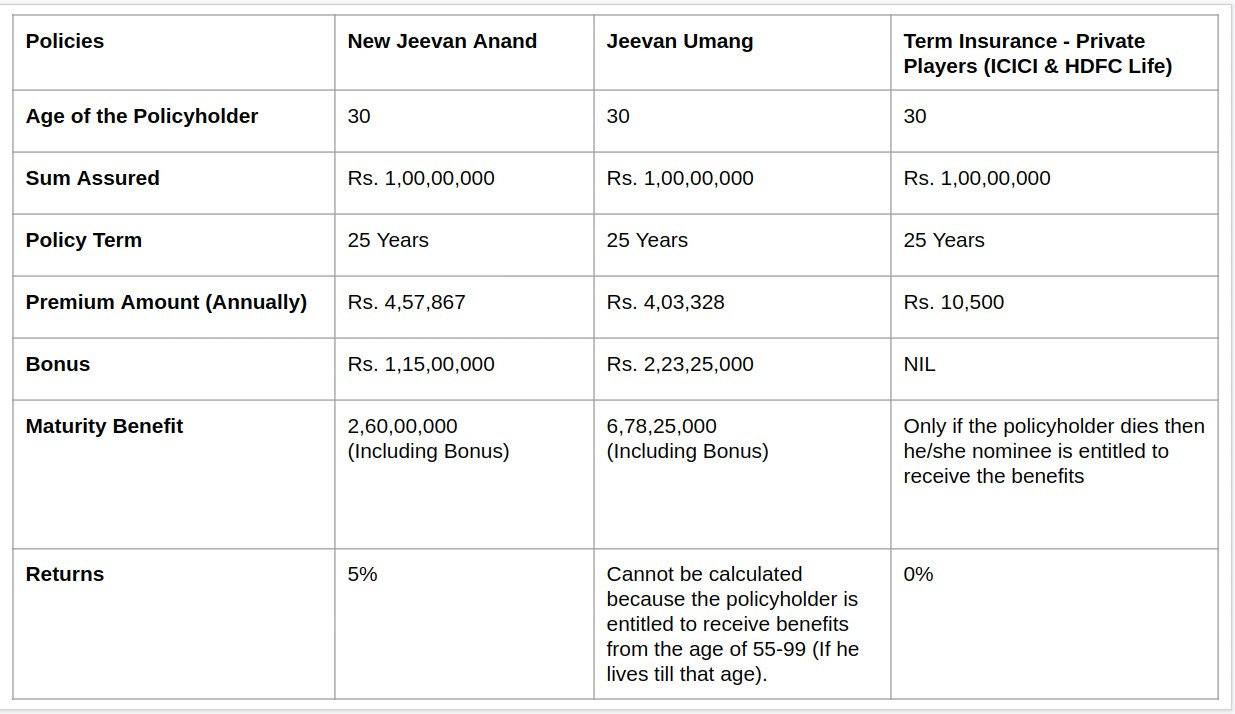

LIC New Jeevan Anand & LIC Jeevan Umang Plan:

Note:

The key idea is to manage our money efficiently by allocating Insurance and Investment separately. DO NOT MIX INVESTMENT AND INSURANCE.

In the above table if you opt for term insurance and paid Rs.10,500 annually then for 25 years totally you would have paid Rs. 2,62,500 only whereas in an endowment plan policy you will be paying Rs. 4,00,000 (Approx) annually then or 25 years then totally you would have paid Rs. 1,00,00,000.

Calculation

Endowment Plan Premium (-) Term Insurance Plan Premium

4,00,000 (-) 10,500

= Rs. 3,89,500

So by opting for term insurance you are saving Rs.3,89,500 per annum and if you invest this money on a cumulative basis for 25 years then you would have gained

Rs. 4,21,36,798 (Assuming that it grows at a rate of 10% Per Annum)

Rs. 5,81,65,567 (Assuming that it grows at a rate of 12% Per Annum)

Rs. 9,53,15,312 (Assuming that it grows at a rate of 15% Per Annum)

Hence it’s very clear that most of the LIC products do not make any sense at all. On the other hand, private players like HDFC Life & ICICI Prudential Life have been focusing on need-based selling over the years3 and the result can be seen in the below image 👇

Since 2016 private players have started to take away market share from LIC4 by focusing on selling protection policies (i.e..Term Insurance), and also it is a most lucrative business as the margins are very high as compared to the savings business which LIC mostly offers.

Why?

Because insurances companies are selling two types of policies which are:

Participating Policies (PAR)

Non-Participating Policies (Non-PAR)

Participating policies allow the policyholder to participate in the profits of the life insurance company.

Non-Participating policies do not allow the policyholder to participate in the profits of the life insurance company.

LIC is focused on selling participating policies thus its profits are shared with the policyholders.

That’s why LIC has very lower profitability than other worldwide insurance companies.

For instance when compared to the Chinese insurance giant Ping An.

Profit numbers5 for Fiscal 2021:

LIC = USD 406 million

Ping An = USD $23.1 billion.

How can LIC improve its profitability 🤔?

By focusing on selling Protection products right?

Yess!

But there is again a problem here.

What problem?

Distribution Mix of LIC:

Agents = 96.42%

Bancassurance = 2.31%

Digital = 0.48%

Agents are the backbone of LIC as they play an imminent role in distributing its insurance products. We saw earlier that for an endowment, money back plan the premium is higher than the term insurance. And insurance agents get a commission from the premium amount which a customer pays and since in the endowment plan the premium amount is higher so they are entitled to get a higher amount of commission than the commission they earn from selling a protection product6.

In the above table, we have clearly seen that in Endowment policies the premium amount is higher compared to the term insurance policies hence LIC agents are heavily incentivized to sell these products.

For LIC Agents:

Higher Premium Amount ➡️ Fixed Commission % ➡️ Higher Commission

Endowment Policy Commission = Rs. 4,00,000 ➡️ 5% ➡️ Rs. 20,000 ✅

Term Insurance Policy Commission = Rs. 10,500 Higher ➡️ 5% ➡️ Rs. 525 ❌

On one hand LIC products are not feasible for policyholders and also it does not create any profits for shareholders and on the other hand if at all they want to change their strategic decision in order to pursuse higher profitable path then it also has barriers because LIC agents are heavily incentivized to sell endowment policies as the commission is higher compared to term insurance policies.

The iron rule of nature is:

“You get what you reward for. If you want ants to come, you put sugar on the floor.”

~ Charlie Munger

Can LIC make the ants to come (i.e..Agents) by not offering enough sugar (i.e.by asking to sell non-participating policies?

Two important questions to ask here if LIC wants to improve its profitability:

How are they going to incentivize their agents to sell protection products when they earn higher commission rates by selling endowment products?

How are they going to convince people for selling protection products instead of investment mixed insurance products (i.e. endowment products) because this is the USP which is used by LIC agents to sell these products?

Conclusion:

I think the above two questions play a key role in determining LIC’s future growth ahead. Although it enjoys an excellent brand recall among the public which keeps floated its business for 6 decades the key question here is whether it can increase the profitability of its business. Because over the long term that’s what the stock market cares about.

Disclosure: Invested in HDFC Life business.

Note:

I’ve not talked about quantitative factors such as comparing Embedded Value (EV), Value of New Business Margin (VNBM), Persistency Ratio, Solvency Ratio, etc., because such comparisons are like comparing apples with oranges.

From LIC Website: https://licindia.in/Products/Insurance-Plan

From LIC DRHP Page No: 181 (Split Differences of Participating policies and Non-Participating policies) & Page No: 191 & 192 (Total number of products that LIC is offering to till date).

From studying both the company’s Annual Report.

From ICICI Prudential Life Annual Report.

Data were taken from this article: https://www.moneycontrol.com/news/business/ipo/lic-3rd-largest-globally-but-offers-highest-roe-of-82-says-crisil-report-8046911.html

Verified from a development manager in LIC that endowment, money back & term insurance commission rates for an agent are SAME.

Disclaimer.

This newsletter is not investment advice or neither advice for buying any insurance products. Any assertions made represent the author’s opinion. The author may own or transact in any securities mentioned. Always do your own research.

Enjoyed this piece? Let me know by hitting the ❤ button.👇 Thank you!

If you enjoy my work, please consider sharing it with friends who might be interested.🙏

Insurance business can't be explained in a simple manner than this article. As profitability is a concern, historical numbers would help readers connect it.

As you rightly pointed out the incentive behind money-back plan, breakup of revenue would help to connect it.

It is a well known fact that LIC works for its agents rather than for its policyholders or even the shareholders (till now GoI) which is not going to change quickly.